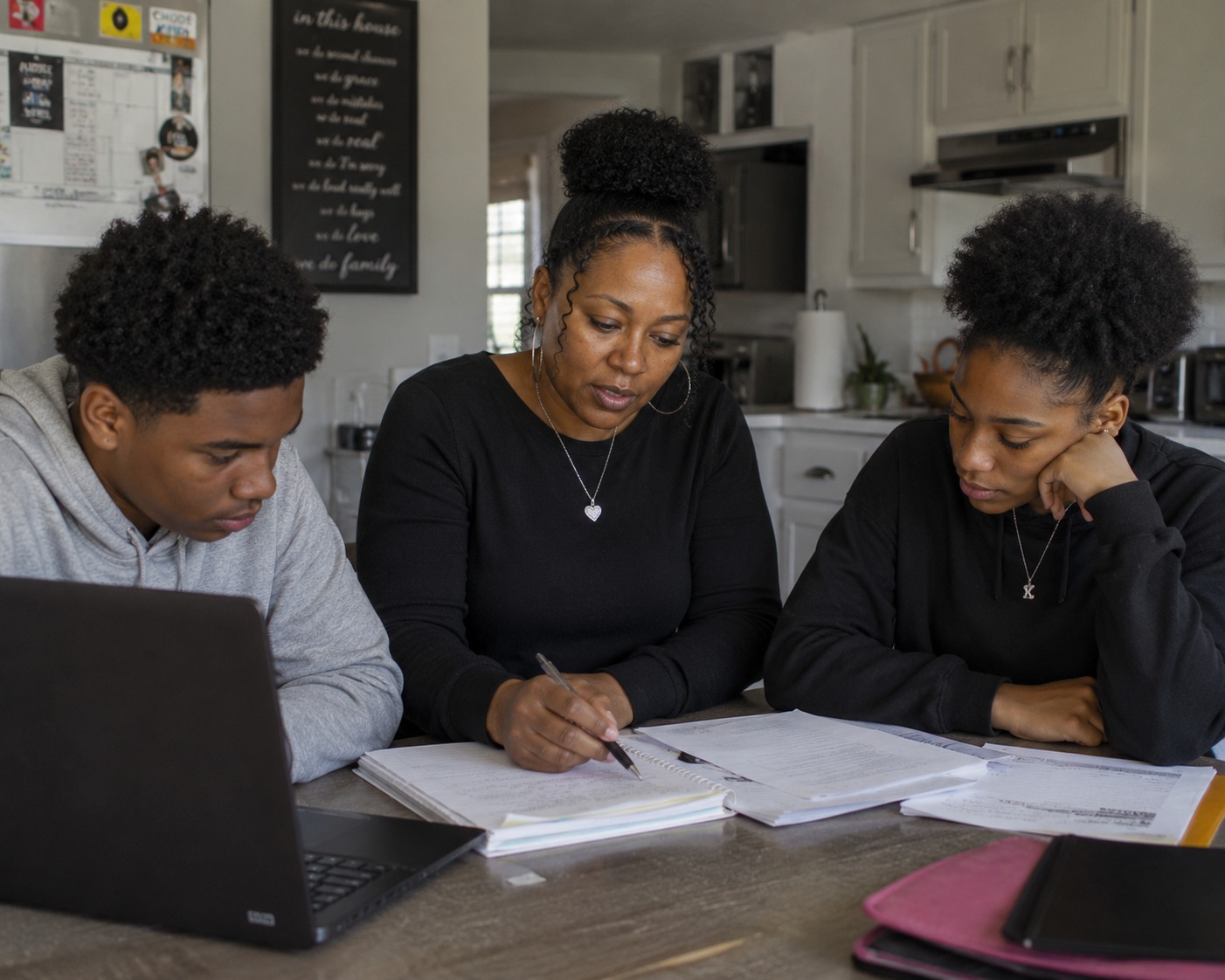

A Marriage Is a Partnership. Your Financial Life Should Be, Too.

For too long, the financial industry treated couples as one client — usually the husband. Wives sat quietly in meetings or did not come at all. Decisions were made between the advisor and one spouse. And then, when something happened — an illness, a death, an unexpected change — the surviving spouse was left with an advisor she barely knew, managing money she had not been part of planning.

That is not how we work, and it is not how the strongest marriages plan.

In the families we serve, both spouses are equal partners in every meeting. Both are present. Both are heard. Both make decisions. Often, the spouse who is home handles more of the day-to-day organization and back-and-forth between meetings — she is the one who follows up, sends the documents, asks the next question. That is a logistical reality of how the family runs, not a sign that one spouse outranks the other in the planning.

When we build a relationship with both of you while you are both healthy, the relationship survives whatever comes next. Neither of you will be left with a stranger.

More Than “Just” a Stay-at-Home Mom

A stay-at-home mom is often the chief operating officer of the household. While her work may not generate a paycheck, it creates tremendous value for her family every day. She coordinates schedules, manages the home, supports her children’s education, and keeps family life moving forward.

Many stay-at-home moms wear countless hats, including:

- Caring for children and managing their daily routines.

- Organizing school activities, volunteering in the classroom, or serving as PTA president or committee leader.

- Coordinating family calendars, appointments, transportation, and extracurricular activities.

- Managing the household budget, paying bills, tracking expenses, and making purchasing decisions.

- Planning meals, overseeing healthcare appointments, and often serving as the family’s financial manager.

These responsibilities require leadership, organization, financial discipline, and long-term thinking—skills that directly contribute to a family’s financial well-being.

Why Retirement Planning Matters for Stay-at-Home Moms

Although a stay-at-home parent may not receive a salary, retirement planning is just as important. Years spent outside the workforce can mean fewer opportunities to contribute toward retirement and lower future Social Security benefits based on personal earnings.

A comprehensive financial plan helps answer important questions such as:

- Are we saving enough for both spouses to retire comfortably?

- Should we contribute to a spousal IRA?

- How will we replace income if something happens to the working spouse?

- Are we adequately protecting our family with life and disability insurance?

- How do we balance today’s family needs while preparing for tomorrow?

Being a stay-at-home mom should never mean sacrificing long-term financial security. Your contributions to your family have lasting value, and your retirement deserves the same thoughtful planning as any income-earning spouse. Financial planning helps ensure that while you’re investing in your family’s future today, you’re also investing in your own.

Comprehensive Wealth Strategy for Your Family

High-earning households generate complex financial decisions. The right advisor coordinates them into one intentional strategy.

Spousal IRA Contributions and Retirement Building

A stay-at-home spouse can still contribute to an IRA in her own name through Spousal IRA rules — building retirement assets independent of her spouse. Most families miss this. We make sure you do not.

Executive Compensation Coordination

If your spouse receives stock options, restricted stock units, deferred compensation, or executive bonuses, those decisions need coordinated tax and investment planning. We work alongside your spouse’s employer benefits and your CPA to integrate these decisions into the bigger picture.

College Planning for Multiple Children

529 plans, custodial accounts, financial aid strategy, the order of operations between college and retirement — we help you fund your children’s education without sacrificing your own future.

Generational Wealth and Inheritance Planning

Inheritance from your parents or your spouse’s parents will reshape your financial picture. We help you plan for it before it arrives — and structure it to protect what your family has built across generations.

Tax-Efficient Investment Strategy

High-earning households face higher tax exposure. Tax planning across investment accounts — Roth conversions, asset location, tax-loss harvesting, charitable giving strategy — can keep meaningful dollars working for your family rather than going to the IRS.

Estate Planning Coordination

Wills, trusts, beneficiary designations, powers of attorney, guardianship for minor children, transfer on death deeds — we coordinate with your estate attorney to make sure your family’s future is protected. Estate planning matters most for high-net-worth families with children, and most families have not updated theirs in years.

Income Replacement and Family Protection

If your family depends on a single income, that income needs to be protected. Life insurance and disability coverage are not just products — they are the foundation that keeps your plan intact if something unexpected happens. We help you size and structure both correctly.

Long-Term Cash Flow and Lifestyle Planning

Lifestyle in your earning years and lifestyle in retirement should be planned together. We build cash flow models that show you what is sustainable, what is aspirational, and how to keep both on track without sacrificing one for the other.

Anticipating Inheritance From Your Parents

For many of the families we serve, the wealth they will eventually manage is significantly larger than the wealth they manage today. Inheritance from parents — yours, your spouse’s, or both — will reshape the financial picture in ways most families do not plan for until the moment arrives. By then, the most important decisions have already been made.

Real coordination begins long before the wealth transfers. We work with families to plan across two generations simultaneously — yours and your parents’ — so that the assets your family has built across a lifetime arrive efficiently, intentionally, and in a structure that protects them.

The conversations we help facilitate include:

Coordinating With Your Parents’ Estate Plan

Are their plans current? Do they use trusts, transfer on death deeds, or beneficiary designations? Are their accounts titled correctly? Small errors in your parents’ estate documents can cost your family hundreds of thousands of dollars at transfer. We help facilitate the conversation, with you and with their professionals.

Lifetime Gifting Strategies

In some situations, lifetime gifts — to children, to grandchildren, to charity — can transfer wealth more efficiently than transfers at death. Annual exclusion gifting, 529 superfunding, irrevocable trust strategies, and charitable giving each have their place. The right strategy depends on your parents’ situation, yours, and the goals of the family.

Stepped-Up Basis and Capital Gains Planning

Most inherited assets receive a stepped-up cost basis at the date of death, which can eliminate decades of capital gains tax. But this only works if the assets transfer correctly. Lifetime transfers, joint titling, and certain trust structures can accidentally forfeit the step-up. We help families avoid those mistakes before they happen.

Aging Parent Care and Asset Protection

If your parents face long-term care needs, the cost can erode the inheritance significantly without proper planning. Medicaid rules, long-term care insurance, and asset protection strategies all need to be considered well before care is needed. Reactive planning is rarely as effective as proactive planning.

Preparing Your Own Family for the Transfer

Receiving inheritance is its own financial event. Sudden additional wealth changes tax brackets, investment strategy, and estate planning needs. We help you prepare your own plan to absorb the inheritance well — so that when it arrives, you are ready, not reactive.

Family Conversations That Matter

The most expensive estate planning mistakes happen because families never had the conversation. Are your parents’ documents current? Do siblings know what is expected? Are there charitable wishes that should be honored? We help facilitate these conversations with care, before silence becomes its own problem.

The right time to plan for inheritance is long before it arrives.

The Quiet Vulnerability Most Families Do Not See

When one spouse leaves the workforce to manage the family, she trades earning years for caregiving years. Those are valuable years — for her family, for her marriage, for her children. But they create real financial vulnerability that most families do not address until it is too late.

No Social Security earnings record. No 401(k) accumulating in her name. No employer life insurance. No disability coverage. No own retirement account growing year after year.

If something happens to her marriage or her spouse — through divorce, illness, or death — the financial picture can shift dramatically overnight. Comprehensive planning during the strong years is what makes the unexpected years survivable. We help families do this work proactively, with intention.

The Financial Value of What You Do

Choosing to stay home and care for children is one of the most important financial decisions a family can make. While a stay-at-home mother may not receive a paycheck, her contributions often support the entire household’s ability to function, earn income, and pursue long-term goals.

Managing a household, caring for children, coordinating schedules, supporting education, overseeing healthcare decisions, and handling countless daily responsibilities creates significant value for a family. If many of these services were outsourced, the cost could be substantial.

Because there is no direct paycheck attached to these responsibilities, many stay-at-home mothers underestimate the financial importance of their role. Financial planning helps ensure that the contributions made today are recognized and protected for the future.

Understanding the Financial Impact of Leaving the Workforce

Stepping away from a career, even temporarily, can affect long-term financial security in several ways. Years spent outside the workforce may reduce future retirement contributions, Social Security benefits, pension accruals, and opportunities for career advancement. While these trade-offs may be worthwhile for many families, they should be understood and planned for intentionally.

Financial planning helps families evaluate how a temporary or long-term career pause may affect future goals, and identify strategies to help bridge potential gaps.

Retirement Planning Still Matters

One of the most common misconceptions is that retirement planning is only important for the spouse earning an income. In reality, stay-at-home mothers are often just as dependent on retirement security as working spouses.

Many families are surprised to learn that retirement contributions may still be possible through a Spousal IRA, even when one spouse is not earning income. Understanding the retirement planning opportunities available can help families continue building long-term financial security while one spouse remains at home. Retirement planning is best viewed as a family goal, not an individual one.

Protecting the Family Against the Unexpected

When families think about insurance, they often focus on protecting the income earner. The loss of a stay-at-home parent, however, can create significant financial and emotional challenges as well. Childcare, transportation, household management, tutoring, meal preparation, and other responsibilities may suddenly require outside assistance.

For this reason, insurance planning should consider the value of both spouses’ contributions to the household — whether those contributions are financial, caregiving, or both. Protecting the family means recognizing the importance of every role within it.

Maintaining Financial Awareness and Confidence

Many stay-at-home mothers manage the day-to-day household finances, while others leave most financial decisions to their spouse. However responsibilities are divided, it is important for both partners to understand the family’s overall financial picture, including:

- Household income and expenses

- Savings and investment accounts

- Retirement plans

- Insurance coverage

- Estate planning documents

- Debt obligations

- Beneficiary designations

Financial confidence grows when both spouses understand the family’s finances and participate in the important planning decisions.

Preparing for Life’s Transitions

No one plans for difficult life events, but financial planning should prepare families for unexpected circumstances. Divorce, disability, job loss, illness, or the death of a spouse can dramatically change a family’s financial situation. Stay-at-home mothers may face unique challenges during these transitions if they have been out of the workforce for an extended period.

Having a financial plan in place can help create greater confidence and flexibility should life take an unexpected turn. Planning is not about expecting the worst. It is about being prepared for whatever the future may bring.

The Importance of Estate Planning

Every family should have basic estate planning documents in place, especially when minor children are involved. These documents help address important decisions regarding guardianship, healthcare, financial management, and the distribution of assets.

Estate planning provides peace of mind that children and loved ones will be cared for according to the family’s wishes.

Building a Family Legacy Together

Financial planning is about more than managing money. It is about creating opportunities, protecting loved ones, and building a strong foundation for future generations. Stay-at-home mothers play a critical role in shaping family values, teaching financial habits, and creating the environment in which children learn about responsibility, generosity, and stewardship. The impact of those contributions often extends far beyond childhood and can influence generations to come.

At Advance Financial Lighthouse, we help families make informed financial decisions that recognize the value of every contribution and support long-term financial strength and independence.

A Practice That Honors the Partnership You Have Built

When you work with Advance Financial Lighthouse, both spouses are full clients. Every meeting includes both of you. Every major decision is reviewed with both of you. Every plan reflects both of your goals, both of your concerns, and both of your voices.

Naturally, we may communicate more often with whichever spouse handles the day-to-day logistics — the documents, the scheduling, the follow-up questions. That is a practical reality of how busy families work, not a hierarchy of importance. The strategic decisions are always made together.

Most clients meet with us at least twice a year for a full plan review, with additional conversations whenever life changes — a job change, a new child, a parent’s illness, a market shift. Between meetings, you can reach our team by phone, email, or video. We respond promptly. Always.

You will not be one of thousands of accounts in a junior advisor’s book. Your plan, your story, and your strategy will be designed and reviewed by people who know your names and your family. And when something changes — for either of you — the relationship continues, because it has always belonged to both of you.

What Stay-at-Home Moms Ask Before Working With Us

Can I open my own retirement account if I do not have earned income?

Yes. Through Spousal IRA rules, a non-working spouse can contribute to a Traditional IRA or Roth IRA based on the working spouse’s earned income. This is one of the most overlooked planning opportunities for stay-at-home moms — and over 20 or 30 years, it can build a meaningful retirement account in your own name.

Will you work with both me and my spouse?

Yes. We work with the marriage, not just one half of it. The strongest financial plans are built when both spouses are at the table, and our practice is designed for couples who want to plan together. Some families prefer every meeting to include both spouses. Others prefer that the partner driving the day-to-day organization meet with us first, then bring conclusions home for shared decision-making. Both approaches work, and both honor the partnership.

Do I need a certain amount of money to work with you?

We work with families across a range of financial situations, with deep experience in households with substantial wealth and complexity. What matters more than the dollar amount is your commitment to thoughtful planning and a long-term partnership. If you are unsure whether we are the right fit, schedule a conversation. We will tell you honestly.

What if I do not feel confident with every financial topic?

No one is expected to know everything. Our role is to translate complexity into decisions you and your spouse can make together. Many of our clients tell us that working with us has made the family’s financial life feel more coordinated and less overwhelming — not because we taught them everything, but because we explained the parts that mattered for their decisions.

Do you serve clients outside Oklahoma City?

Yes. While we are based in Oklahoma City, we serve clients across Oklahoma and nationwide. Most meetings are held by video, with the same depth of conversation and the same quality of planning regardless of location.

Other Ways We Serve Families in Oklahoma City

· Financial planning for women in every season of life

· Family financial planning for households in their peak earning years

· Retirement planning for couples planning the next chapter together

Steady. Purposeful. Always in your corner.

Schedule a confidential conversation. There is no fee, no obligation, and no commitment to continue.

Schedule a Conversation Call (405) 843-2380